Inflation increased due to multiple factors, namely expansionary economic policies (monetary and fiscal) during the pandemic that increased demand amid market shortages and trade restrictions, which raised transport costs, and Russia’s invasion of Ukraine, which raised energy and food prices.

Publication date

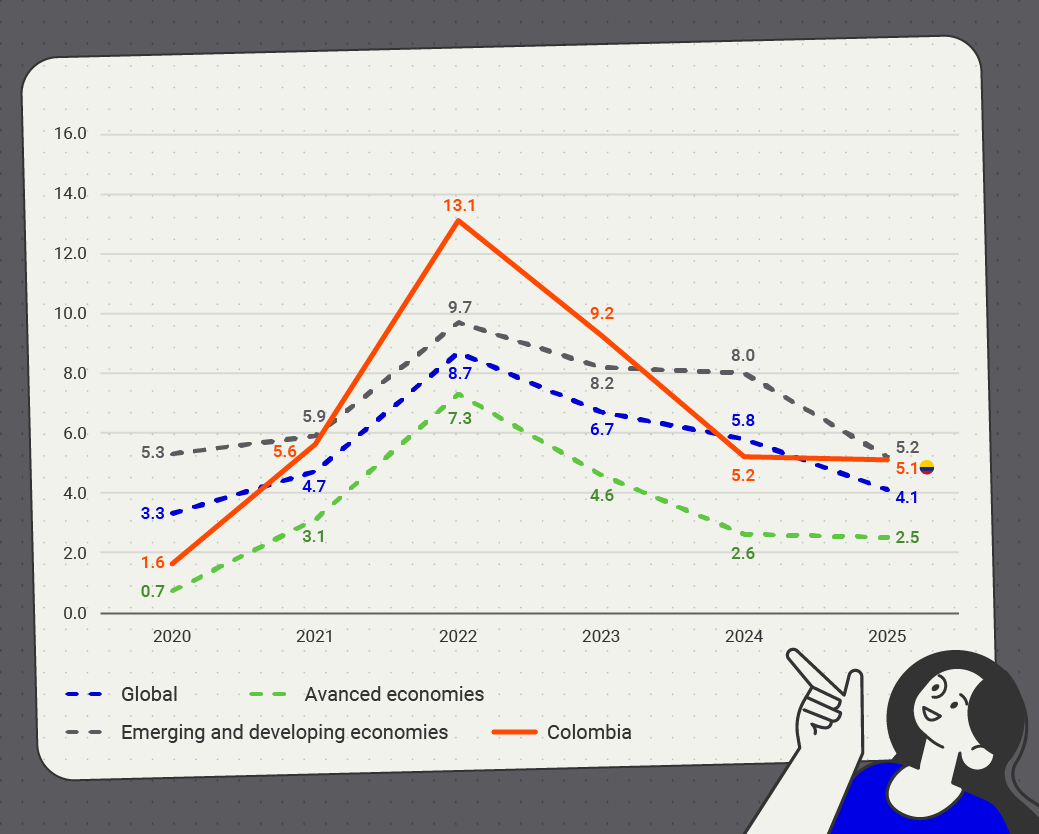

After a prolonged period of price stability, global inflation rose in 2021 and 2022 to unexpectedly high levels, reaching an average of 8.7% in 2022. In advanced economies, average annual consumer inflation increased from 0.7% in 2020 to 7.3% in 2022, while in emerging and developing economies it rose from 5.3% to 9.7% (Graph 1).

Global inflationary pressures arose from a combination of shocks, several of which occurred simultaneously. The COVID-19 pandemic led many countries to adopt expansionary monetary and fiscal policies aimed at supporting households and businesses in confronting its effects. In tandem, stringent restrictions imposed on the international mobility of goods led to a significant increase in maritime transport costs. The resultant demand stimulus from the generous policy measures under market-shortage conditions led to significant inflationary pressures that became evident in 2021. The situation was further aggravated by Russia’s invasion of Ukraine in February 2022, which generated significant increases in oil and gas prices and restricted the supply of cereals and fertilizers, placing upward pressure on food prices.

Accordingly, by 2022, inflation had become a worrying problem for central banks, as observed inflation and their expectations deviated from the established targets. This phenomenon was met with increases in policy interest rates in both advanced and emerging economies, leading to the most widespread global monetary policy tightening on record. Consequently, almost as quickly as it had risen, global inflation began to ease, averaging 6.7% in 2023 and continuing its decline to 5.8% in 2024 and 4.1% in 2025. In advanced economies, average inflation decreased to 4.6% in 2023 and stood at approximately 2.5% in both 2024 and 2025. In emerging and developing economies, average inflation fell to 8.2% in 2023, remained elevated at 8.0% in 2024, and declined further to 5.2% in 2025..

In the context of the aforementioned shocks, inflation in Colombia increased from 1.6% at the end of 2020 to 13.1% at the end of 2022 (Graph 1). The increase in inflation in Colombia was more intense than that observed in the rest of the world, pointing to the presence of idiosyncratic factors specific to the Colombian economy that exerted further upward pressures during this period. This phenomenon was analyzed in a previous blog on the determinants of the post-pandemic inflationary surge, which identified specific features of the Colombian economy which identified several country-specific factors explaining differences in price dynamics between Colombia and other economies. These include the road blockades in May and June 2021, which disrupted food production and distribution; the sharp depreciation of the Colombian peso in 2021 and 2022; and the reversal of temporary gas price relief measures, as well as taxes and fees that had been suspended during the pandemic

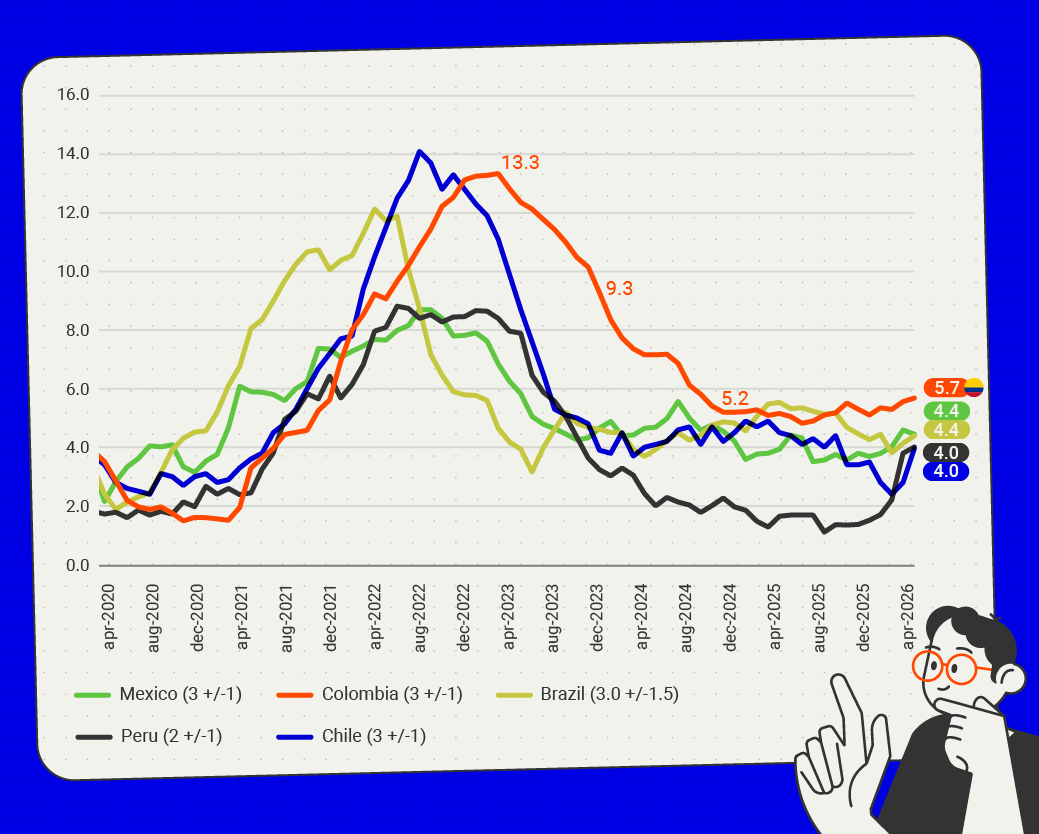

* Due to heterogeneity across countries, the series for country groupings represents the annual average inflation for each year. For Colombia, the series corresponds to year-end inflation.

With the previous framework in mind, it is useful to compare inflation behavior in Colombia within the Latin American context. To this end, Graph 2 shows monthly inflation in Colombia and in its main Latin American peers between April 2020 and April 2026. As can be seen, in the post-pandemic period, Colombia experienced a strong inflationary shock, similar in magnitude to those observed in Chile and Brazil. However, in Colombia inflation proved more persistent: although it declined from the peak of 13.3% reached in March 2023 to 9.3% in December of that year, it remained well above the 3.0% target. By contrast, other countries managed to bring inflation closer to their respective targets in 2023. In 2024, inflation in Colombia continued to decline to 5.2% in December but remained above that of comparable countries in the region, and in 2025 it stabilized at slightly above 5.0%. In the first months of 2026, inflation in Colombia increased again, diverging from its regional peers, in an environment of notable fiscal expansion and strong labor cost pressures.

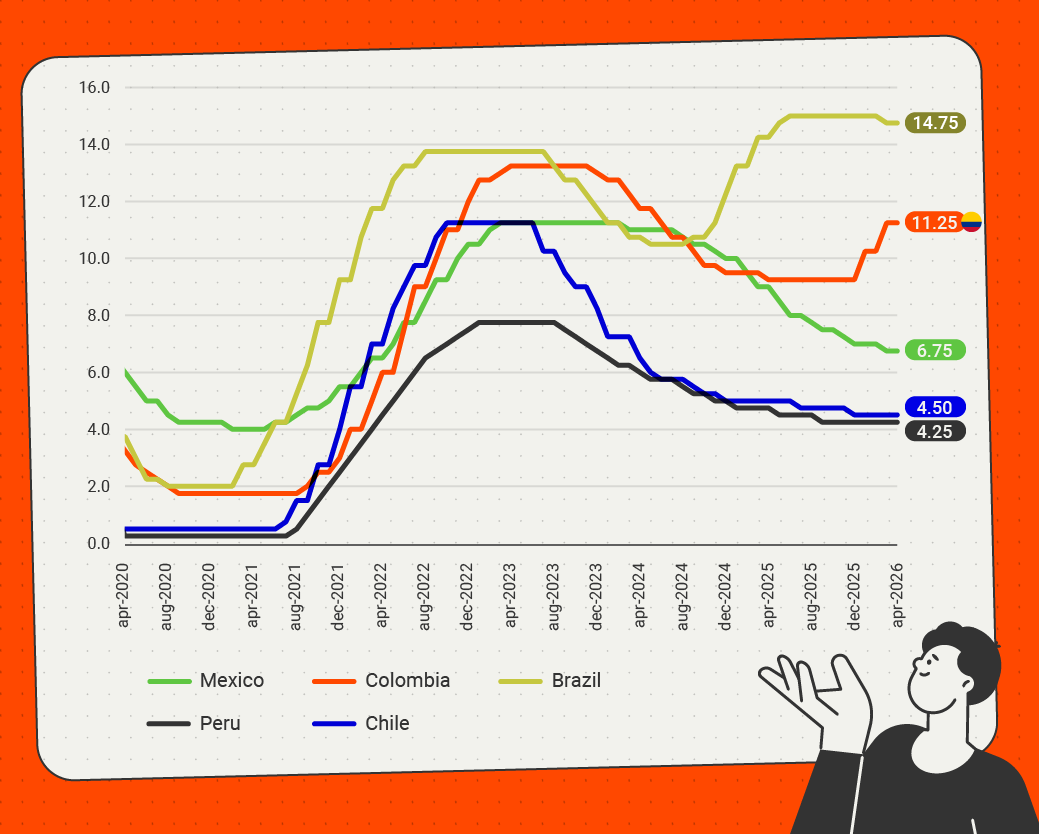

The variation in Colombia’s inflation behavior relative to that of its Latin American peers is also reflected in the different handling of the monetary policy interest rate by the central banks (Graph 3). To underscore, both Colombia and Brazil have had to raise their policy interest rates the most to bring inflation closer to their targets. Brazil has been successful in this effort, as its April 2026 inflation rate of 4.4% falls within the accepted +/-1.5% range around its target of 3.0%. Mexico, Peru, and Chile have been able to reduce and maintain stable policy rates recently, thanks to inflation rates close to their targets.

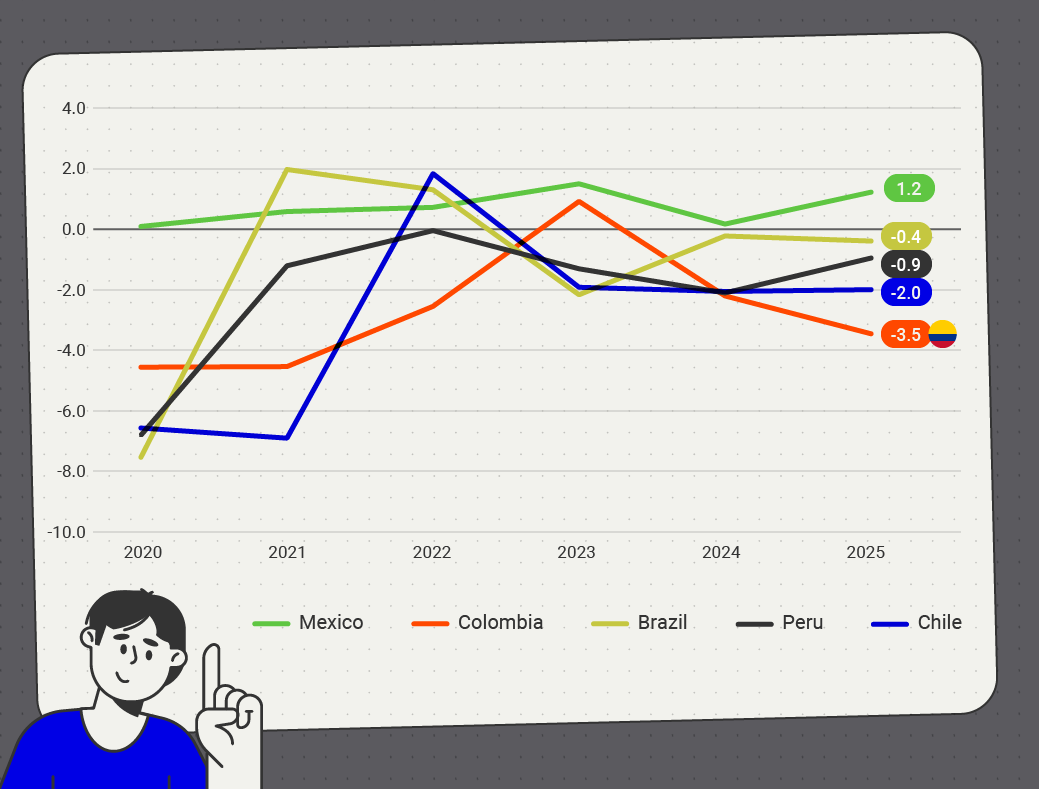

Lastly, an additional factor that has led Colombia to maintain relatively high monetary policy interest rates is the widening fiscal imbalance, as reflected in the upward trend of the general government primary deficit, in contrast with the behavior of its Latin American peers. This tends to stimulate domestic demand, making it more difficult for inflation to converge to its target and requiring a more restrictive monetary policy stance (Graph 4).